This Isn’t Stagflation — It’s A Liquidity Shock (Here’s The Difference)

TL;DR (For Skimmers)

- Real yields (not headlines) drive the dollar and gold

- When real yields rise → USD strengthens → gold struggles

- Today’s move (stocks ↓, yields ↑, USD ↑, gold ↓) looks like a liquidity / VAR shock — not a structural regime shift

- The deeper macro backdrop (rising debt, labour revisions, future rate cuts, liquidity constraints) hasn’t changed

- If this becomes prolonged, policy response matters more than missiles

Now let’s unpack it properly.

Markets feel chaotic right now.

Stocks are down sharply. Bond yields are rising. The dollar is strengthening. Gold spiked… and then sold off hard.

If you only read headlines, it feels like stagflation is here — rising inflation combined with low job growth.

But markets don’t move off headlines. They move off plumbing.

Let’s simplify what’s happening — and then I’ll tell you what I actually think is driving this move.

The Simple Framework: Real Yields Drive Everything

When people say “the 10-year yield is 4%”, that’s the nominal yield.

But the number that really matters is:

Real yield = Nominal yield − Inflation expectations

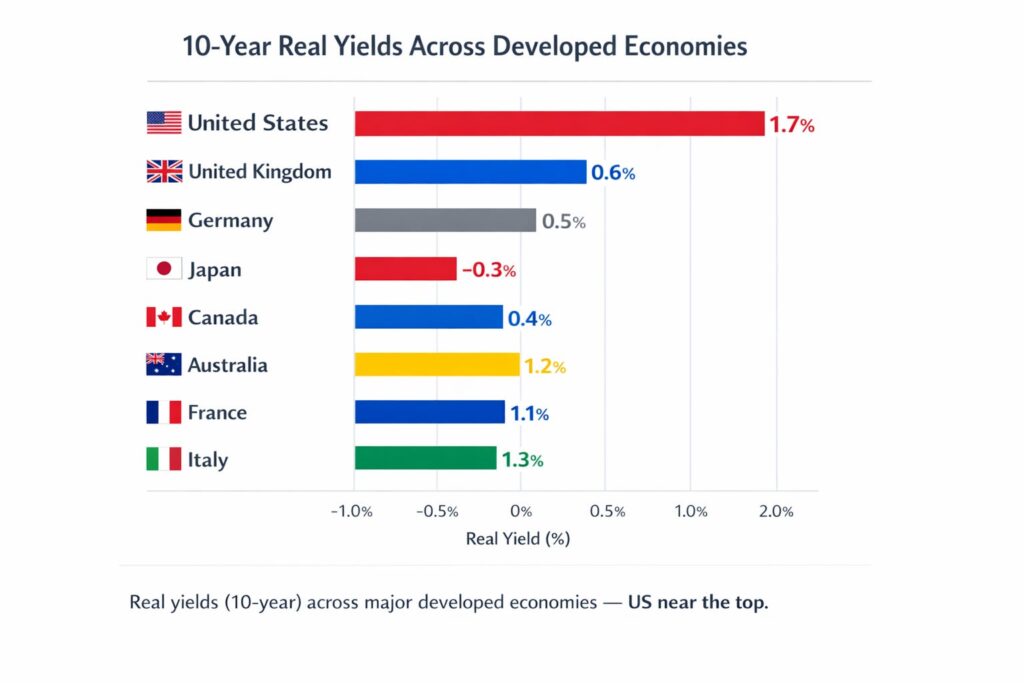

If the 10-year yield is 4% and inflation expectations are 2.3%, then the real yield is 1.7%. That 1.7% is what investors truly earn after inflation.

Why does this matter? Because global capital constantly asks: “Where can I earn the safest real return?”

Right now, the US offers one of the highest real yields in the developed world. That supports the dollar.

And when real yields rise:

- The dollar tends to strengthen

- Gold tends to struggle

- Financial conditions tighten

That’s the mechanical relationship.

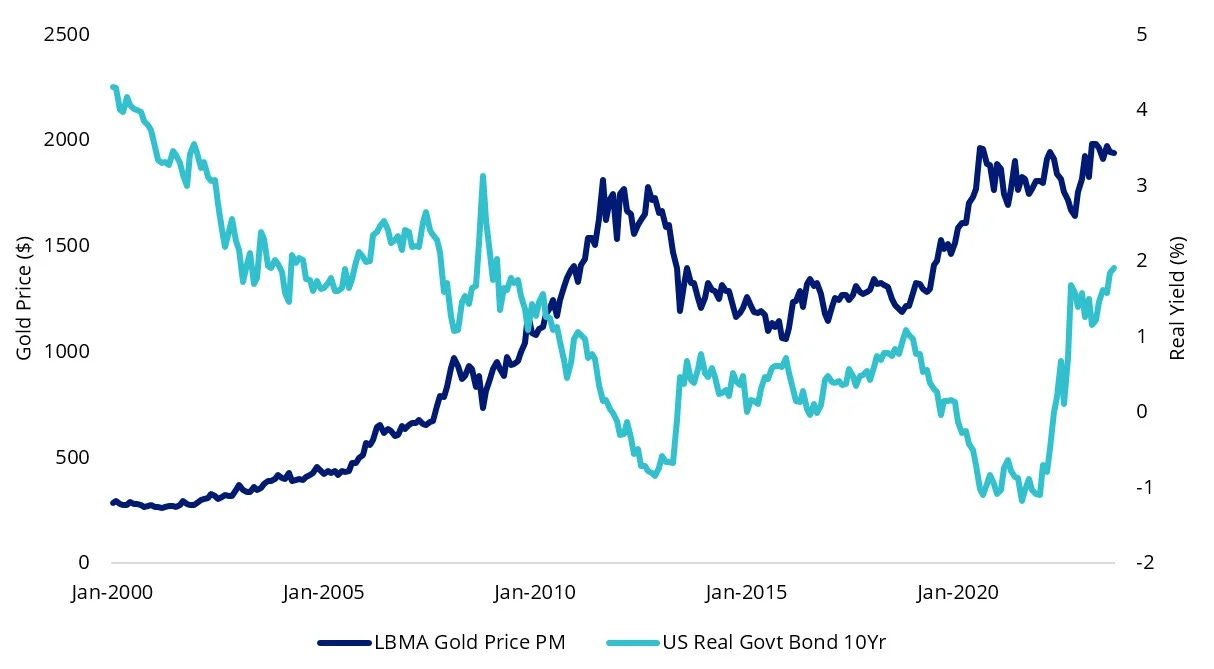

Why Gold Often Moves The Opposite Way

Gold doesn’t pay interest.

So when bonds offer a strong real return — say +2% — gold looks less attractive. But when real yields fall — or turn negative — bonds lose their appeal. That’s when gold shines.

Historically:

- Rising real yields → pressure on gold

- Falling real yields → support for gold

So What Does This Mean For The Market Today?

Here’s what we’re seeing:

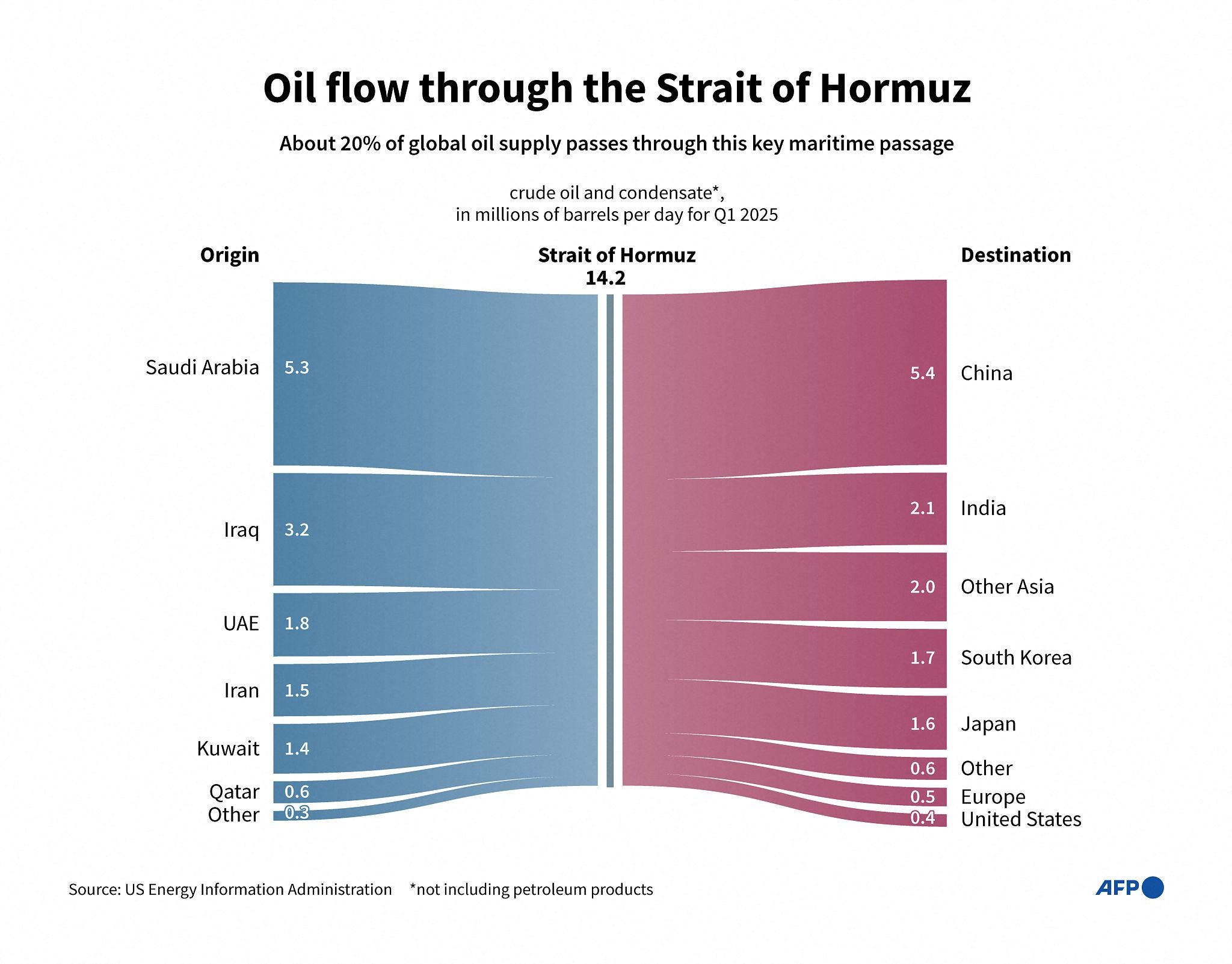

- Oil is up sharply on Hormuz risk — roughly 20% of global oil passes through it

- Stocks are down

- Bond yields are up

- The dollar is up

- Gold is down significantly

If this were a clean inflation panic, we would likely see:

- Breakeven inflation exploding higher

- Real yields falling

- Gold outperforming

But instead:

- Nominal yields are rising

- Real yields appear to be ticking up

- The dollar is strengthening

- Gold is being sold

That combination looks more like stress.

If I Had To Choose — What’s Driving This?

If you forced me to pick the most likely explanation:

This looks like a liquidity shock / VAR shock / deleveraging event.

Oil spikes → volatility spikes → risk models tighten → leverage gets cut.

When funds reduce risk, they sell what they can. What’s liquid?

- Stocks

- Bonds

- Gold

Gold is one of the most liquid assets in the world. It often gets sold to raise cash or meet margin requirements.

Stocks down. Bonds down (yields up). Gold down.

That’s a liquidity flush profile. Not yet a monetary regime shift.

What’s Changed?

Very little, structurally.

Before Iran, the backdrop already looked like this:

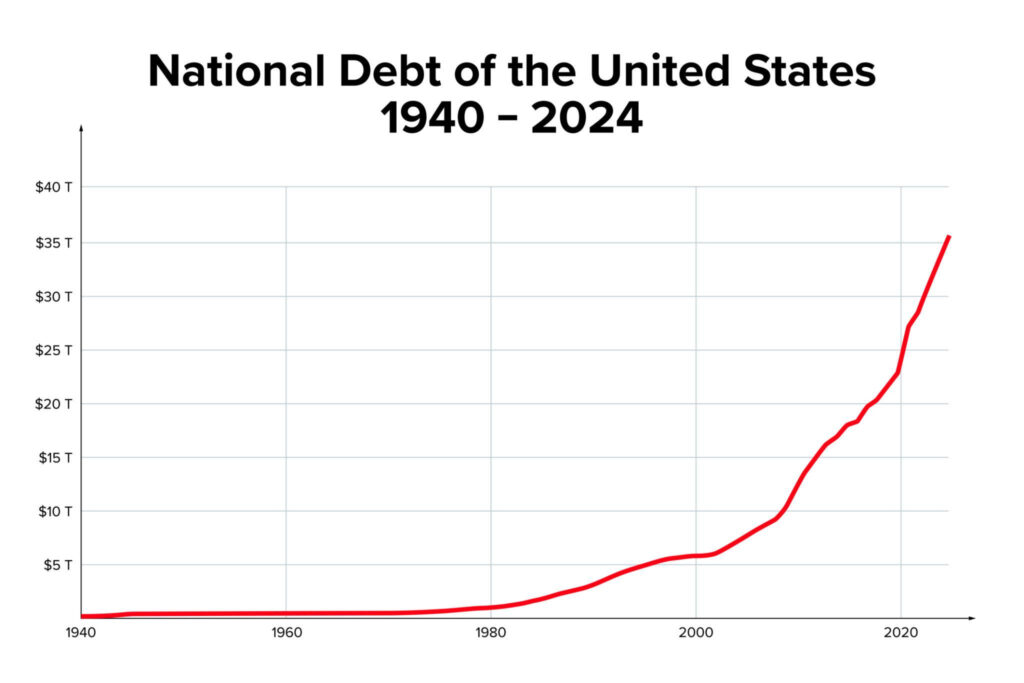

- US government debt continues to climb

- QT ended in December 2025 — because liquidity stress was building

- Repo balances are depleted

- China continues reducing Treasury holdings

- Labour market data has seen consistent downward revisions

- Growth isn’t strong

- Political pressure on Powell to cut rates is intensifying

None of that disappeared because of a missile strike. It’s just temporarily overshadowed.

The Broader Undercurrent Still Exists

Fiat currencies continue to lose purchasing power over time. Deficits remain structural. Rate cuts are still likely in the future if growth weakens further. If stress builds enough, QE always re-enters the conversation.

That macro backdrop hasn’t changed.

Could This Become Something Bigger?

Yes.

If Hormuz were closed for an extended period:

- Oil spikes further

- Inflation pressure builds

- Growth slows

- Policy gets trapped

But markets move in phases:

- Phase 1: Liquidity shock

- Phase 2: Growth damage

- Phase 3: Policy response

Gold usually performs best in Phase 2 and 3. Right now, this looks like Phase 1.

And What About Trump?

My view: Trump is a deal maker.

His stated objectives are clear:

- Lower gas prices

- Lower inflation

- A weaker dollar

- Stronger US trade positioning

Sustained escalation that drives oil higher works directly against those goals. History suggests leverage first, negotiation later.

My base case: this ends in negotiation, not sustained Iraq-style intervention. Timing is uncertain. But incentives matter.

Final Thoughts — And A Question For You

Right now, markets feel like they’re breaking.

But ask yourself: are we seeing a structural monetary reset? Or are we watching a fast, violent liquidity squeeze that forces positioning adjustments before fundamentals reassert themselves?

The answer to that question determines everything.

So I’ll leave you with this:

If real yields start collapsing and the dollar rolls over — that’s your signal the regime is changing.

Until then, I’m watching liquidity.

What do you think this is? Liquidity event — or something more structural? Let me know in the comments.

This article is for informational and educational purposes only. Nothing here constitutes financial advice. Always conduct your own research and consult a qualified financial adviser before making any investment decisions.

Get the next piece delivered direct to your inbox.