The violent sell-off in gold and silver has left many traders confused.

Gold fell hard.

Silver collapsed.

The dominant explanation making the rounds is simple:

“Markets sold precious metals because Trump nominated a new Fed Chair perceived to be hawkish.”

At face value, that sounds logical.

But when you step back and examine debt, liquidity, geopolitics, and institutional constraints, the conclusion becomes clear:

This was not a fundamental shift.

It was a positioning and liquidity shock inside a much larger secular trend.

The Headline Narrative vs the Reality

Markets reacted to the idea that a new Fed Chair might be “hawkish.”

That reaction assumes three things:

- The Fed has real freedom to be hawkish.

- Trump wants tight monetary policy.

- The long-term monetary backdrop has improved.

None of those assumptions hold.

Trump, the Fed, and Political Reality

Let’s be clear.

Donald Trump does not want:

- Higher rates

- A stronger dollar

- Rising unemployment

- Tight financial conditions into an election cycle

We know this because of his views towards Fed Powell after each press conference and his push for Powell to cut rates.

Higher rates:

- Inflate debt-servicing costs

- Pressure equities

- Damage labour markets — as we’ve seen in the consistent downward revisions to jobs data throughout 2025

That is politically toxic.

While Trump can nominate a Fed Chair, he cannot override economic reality. Monetary policy remains constrained by data, debt, and financial stability — not personality.

A hawkish nomination does not create room for sustained tightening.

The Fed Is No Longer Free — It’s Subordinate to Debt

This cycle is fundamentally different from previous gold cycles.

In past rallies, debt spikes were cyclical phases:

- Wartime spending

- Financial crises

- Temporary fiscal blowouts

Today, debt is structural:

- The US runs ~7% of GDP deficits in peacetime

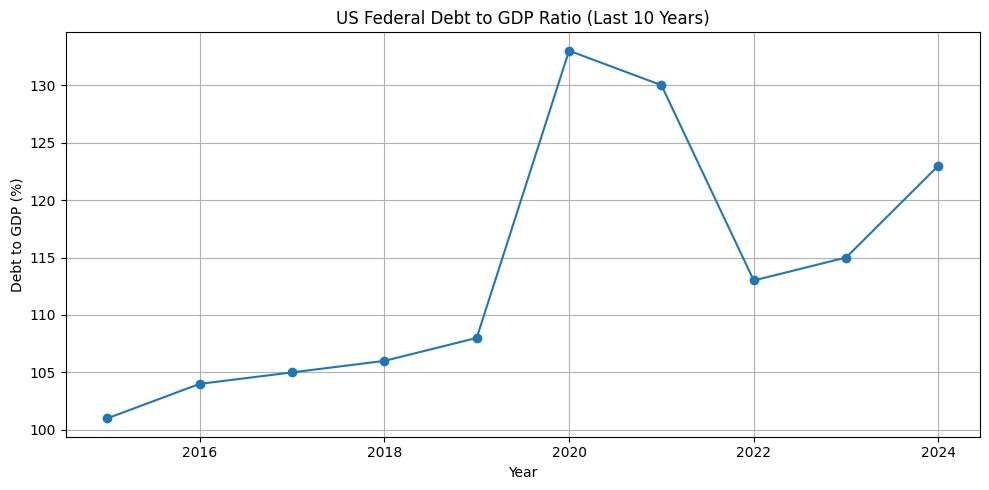

- Debt exceeds 124% of GDP

- There is no credible path to fiscal consolidation

This subordinates monetary policy to fiscal reality.

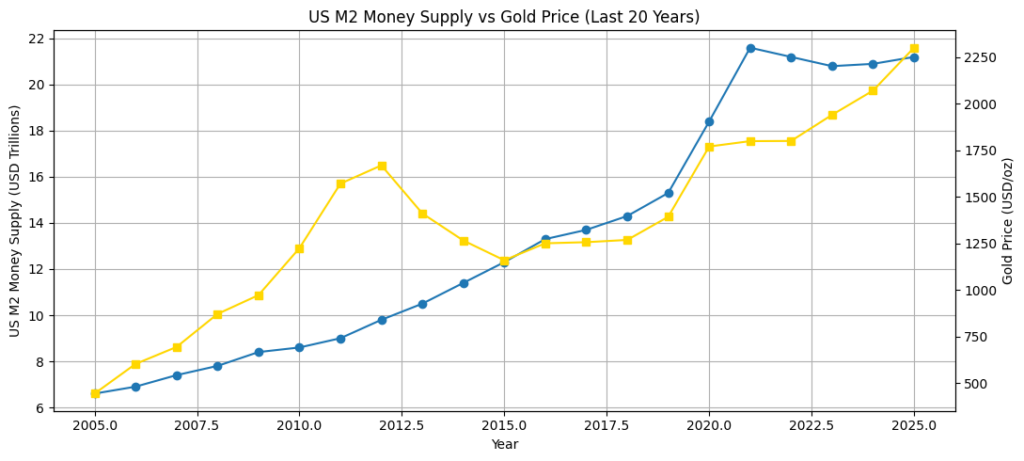

That is a classic precondition for long-term currency debasement — not just over years, but over decades. Which is why the USD has lost 99% of its value against gold since being de-pegged in August 1971.

Why This Is Not the 1970s

The comparison to the 1970s is common — and misleading.

In the 1970s:

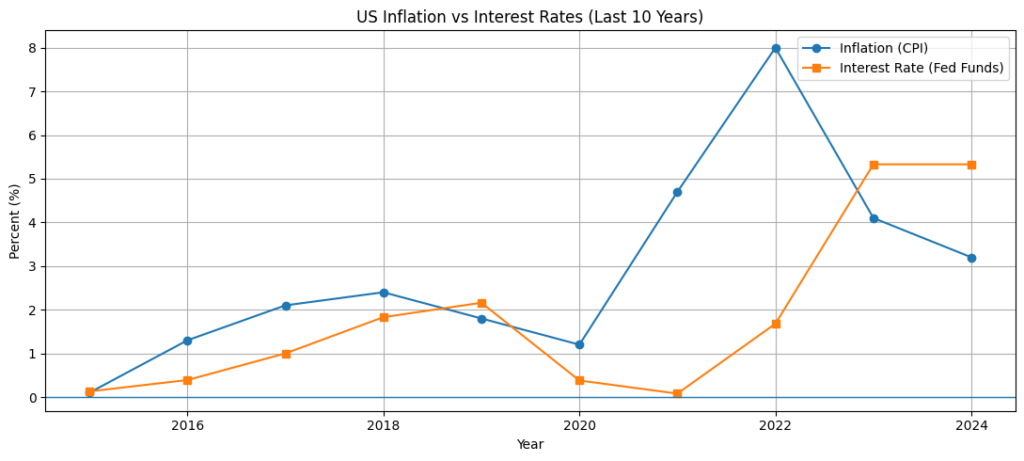

- Inflation was high (double digits)

- US debt was under 40% of GDP

- The Fed could hike aggressively — and they did

In the 1970s, gold surged for very specific reasons. In 1971, the US dollar was de-pegged from gold, ending the Bretton Woods system. This meant gold was no longer fixed to the dollar and could trade freely for the first time. At the same time, US citizens had not been allowed to own gold bullion since the 1930s. That ban was finally lifted in 1974, just as inflation was already running hot. So you had three powerful forces coming together:

- High inflation — the public invested as a hedge

- A freely trading gold price

- The public suddenly allowed to invest in gold, having been banned since 1934 via the Gold Reserve Act

That combination led to strong and sustained demand, which pushed gold sharply higher throughout the 1970s.

The rally ended when Federal Reserve Chair Paul Volcker raised interest rates to nearly 20% to crush double-digit inflation. Those rate hikes caused a deep recession but successfully brought inflation under control. Once inflation was beaten and cash started offering high real returns again, investors no longer needed gold as an inflation hedge. That’s why gold peaked around 1980 and then entered a long decline.

Today:

- Inflation remains sticky

- Debt is ~124% of GDP

- Aggressive hikes would destabilise the Treasury market

Volcker-style tightening is no longer feasible. The constraint is debt, not willpower.

Liquidity Reality: Repo Stress and the End of QT

Two underappreciated dynamics matter here.

- Repo and reserve buffers are already low. Low repo liquidity reduces the system’s ability to absorb shocks — which explains why sell-offs are so violent, but also why policy support becomes inevitable.

- QT ended in December 2025. Ending Quantitative Tightening:

- Stabilises bank reserves

- Reduces Treasury absorption pressure

- Improves liquidity at the margin

Historically, gold responds more to liquidity regime shifts than to the first rate cut itself. Prolonged hawkishness is incompatible with this setup.

Quantitative tightening had to end because it was removing too much liquidity from the system after pumping so much in during the pandemic. As the Fed shrank its balance sheet, cash reserves fell while banks were forced to absorb more government bonds. This left the system short of usable cash and increased the risk of funding stress, making continued QT unsustainable.

Flows vs Fundamentals: Why Price Can Mislead

Markets don’t trade regimes day-to-day — they trade flows.

This move was driven by:

- Crowded positioning and overbought RSI signals

- Leverage and margin calls — especially in silver

- CTA and trend-following selling

- Volatility targeting de-risking

- A short-term upside USD squeeze after excessive selling

This was a liquidity event, not a thesis failure.

Short-term price action often reflects who is forced to sell — not what is fundamentally wrong.

Geopolitics Changed the Gold Equation Permanently

The post-2014, and especially post-2022, world is structurally different.

Sanctions on Russia and frozen reserves changed how sovereigns view safe assets. Many countries now recognise:

- US Treasuries are not politically neutral

- Access can be revoked — for example Russia being locked out of the SWIFT banking system in response to the Ukraine invasion

- Reserves can be frozen

Gold, by contrast:

- Has no counterparty

- Is nobody’s liability

- Cannot be sanctioned

This dynamic did not exist in the 1970s or even in 2008. That is why countries such as China, India, Turkey, and Saudi Arabia are accumulating gold — often quietly and methodically.

This isn’t about yield. It’s about sovereign optionality.

Tariffs, Coercion, and the Push to Build Alternatives

Trump’s tariff strategy has been openly transactional:

- Threaten aggressive tariffs

- Apply pressure

- Extract concessions

- Partially roll them back

From a negotiating standpoint, it can work. From a global system standpoint, it changes behaviour.

Tariffs are increasingly perceived as economic coercion, not neutral trade tools. That creates two risks for other countries:

- Unpredictability

- Dependence

Rational sovereigns respond by reducing exposure — not by abandoning the dollar overnight, but by:

- Expanding bilateral trade

- Settling more trade in local currencies

- Building regional trade blocs

- Exploring non-USD payment rails

This is especially visible among BRICS nations, but not limited to them.

Gold increasingly functions as:

- Settlement collateral

- Reserve diversification

- A neutral bridge asset

Trump didn’t create this trend — but erratic, coercive trade policy accelerates it.

De-Dollarisation: Slow, Real, Structural

The dollar remains dominant — but the trend matters.

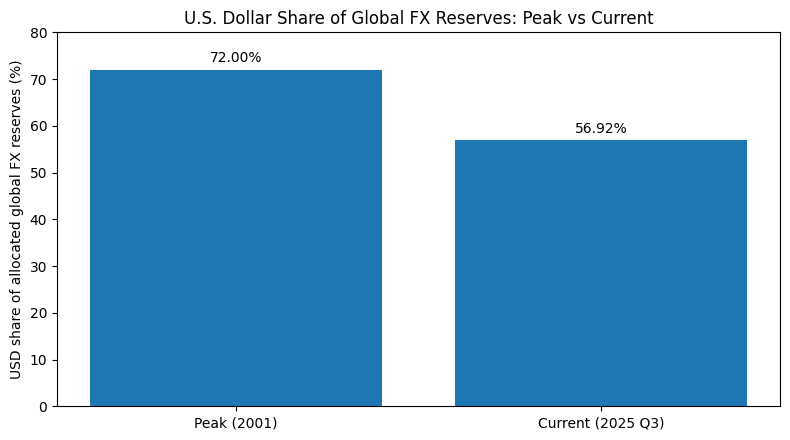

USD share of global FX reserves:

- ~72% in 1999

- ~57% today

In prior cycles, there was no credible alternative to the USD system. Today, there is at least the beginning of one. Gold sits at the centre of that transition.

Central Banks and ETFs Buying Together Is New

In 2011:

- Gold demand was ETF-driven

- Central banks were net sellers

Today:

- Central banks are persistent net buyers since 2014

- ETFs are buying alongside them

This alignment has never existed in modern history. It materially deepens and stabilises demand.

China runs a closed-loop gold system. Gold imports flow into China, but exports since 2014 are tightly restricted and rarely permitted. With domestic mine production of around 380 tonnes per year, plus substantial imports, China steadily absorbs physical gold from global markets.

The Global Debt Constraint

Global debt now exceeds 350% of GDP. That reality:

- Limits the ability to maintain high real rates

- Forces financial repression

- Tolerates inflation above bond yields

This is the environment where gold structurally outperforms.

What Would Actually Break the Gold Thesis?

A strong investment view isn’t about being bullish forever — it’s about knowing what would make you change your mind.

For gold, the long-term case would only really weaken if several of the following happened at the same time:

(A) Governments seriously get their finances under control

- Budget deficits fall year after year

- National debt starts shrinking relative to the size of the economy

- This would show governments no longer need to rely on money printing to fund themselves

(B) Central banks stop buying gold and start selling it

If central banks no longer felt the need to hold gold and instead reduced their holdings, it would suggest confidence had returned to paper currencies and government bonds.

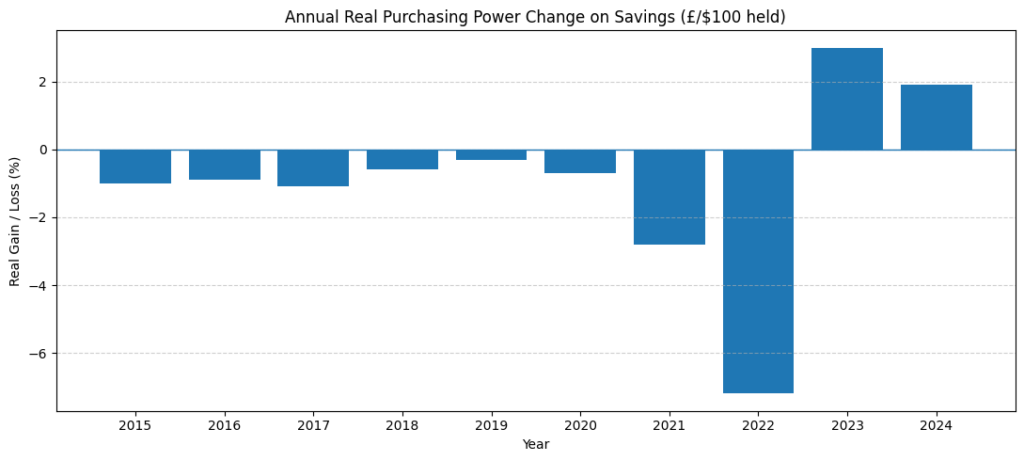

(C) Inflation stays below interest rates for a long time

- Savings and bonds earn more than inflation

- Cash holds its value without causing economic stress

- This would remove one of the main reasons investors turn to gold

(D) Global debt levels meaningfully fall

- Countries reduce their overall debt burdens

- The world moves away from borrowing-led growth

- That would ease pressure on central banks to keep money loose

(E) Global politics become more stable and cooperative

- Sanctions are rolled back

- Frozen reserves are returned

- Countries feel safe holding each other’s assets again

- We move more towards world peace and less war and aggression

- This would reduce the need for neutral assets like gold

(F) Strong economic growth without inflation

- Economies grow because of productivity, not debt

- Living standards rise without money losing value

- This would be a healthy backdrop for financial assets and reduce demand for gold

None of these conditions are in place today. Until they are, short-term price swings don’t invalidate the bigger picture — they’re just part of the journey.

The Trump-Fed Paradox

Here’s the irony markets struggle with.

A hawk cutting rates is more credible than a dove cutting rates — it looks better to the public and investors. We know Trump wants lower rates, hence his repeated comments towards Fed Powell.

By nominating a perceived hawk:

- Fed independence is signalled

- Markets tighten voluntarily

- Inflation optics improve

- The inevitable cuts will feel authentically data-driven instead of looking coercive

But when labour, liquidity, and debt realities reassert themselves, the pivot becomes unavoidable — and politically defensible.

Historically, that’s when precious metals perform best.

Final Takeaway

Nothing fundamental broke.

- Debt dominance worsened

- Liquidity constraints tightened

- Geopolitical fragmentation deepened

- Monetary flexibility narrowed

This sell-off was:

- Emotional

- Flow-driven

- Timing-related

Not structural.

The destination hasn’t changed — only the path the market thinks it will take. And structurally, that path still favours gold and silver.

This article is for informational and educational purposes only. Nothing here constitutes financial advice. Always conduct your own research and consult a qualified financial adviser before making any investment decisions.

Get the next piece delivered direct to your inbox.